Brisbane-based Vaxxas has raised ~A$90m (A$49.22m Series D equity plus a A$40m debt facility), extending its cash runway into the second half of 2027, and triggering a leadership hand-off as founding CEO David Hoey moves into a strategic advisor role while the board completes a global CEO search. The round was led by SPRIM Global Investments with participation from new backer LGT Crestone and existing investors OneVentures and Brandon Capital–Hostplus. The company says proceeds will fund late-stage readiness for its high-density microarray patch (HD-MAP) platform, including semi-automated manufacturing lines.

Why this matters now

Vaccine delivery has barely changed in a century: liquid doses, cold chain, trained vaccinators, a needle and a syringe. That logistics model worked—until it didn’t. The COVID era exposed raw spots from fill-finish bottlenecks to sharps supply. In post-mortems, U.S. and global reviews pointed at downstream constraints—cold chain, staffing and consumables—just as much as upstream antigen production. Any technology that trims those friction points is no longer a curiosity; it’s policy-relevant infrastructure.

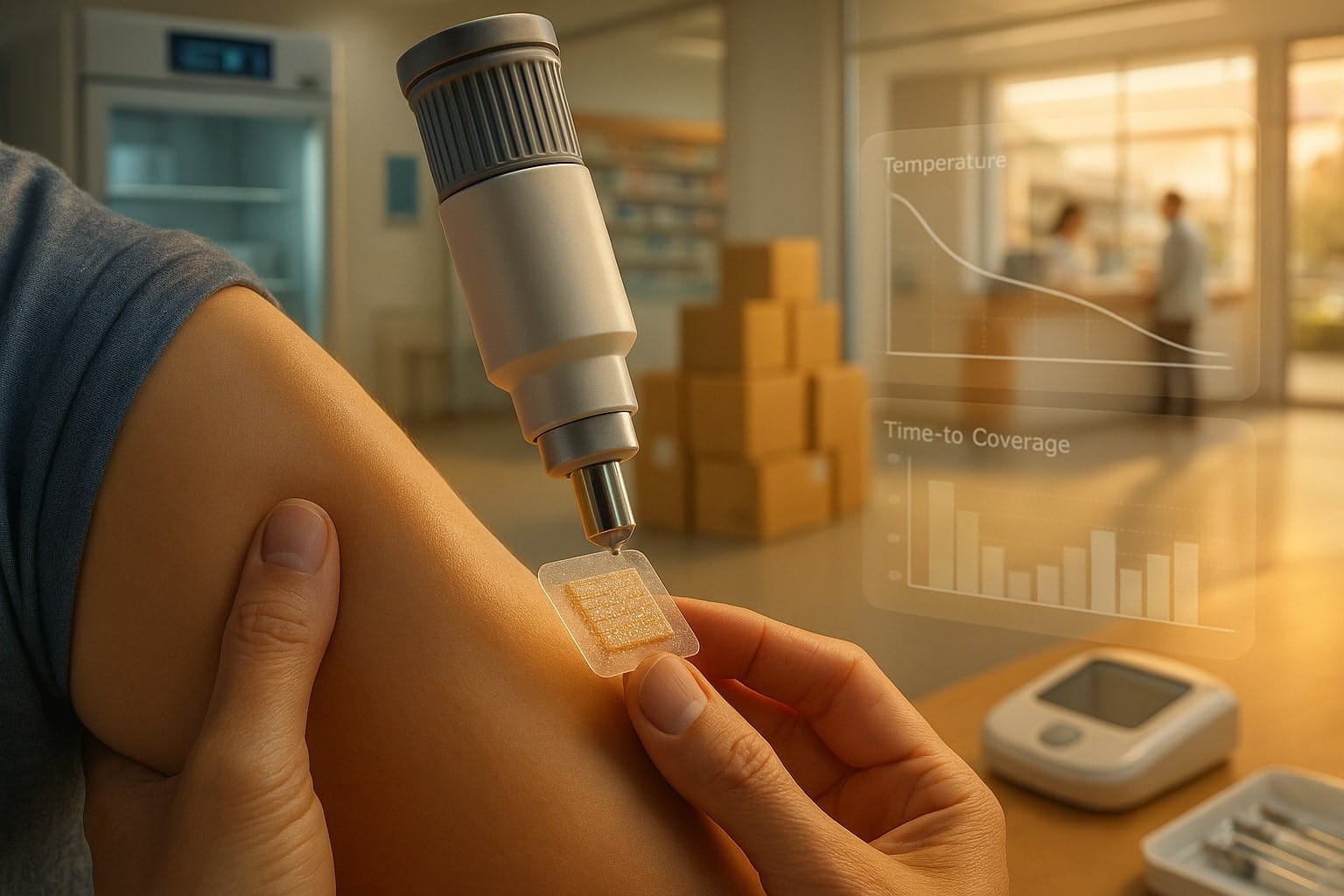

Vaxxas’s pitch is that a postage-stamp-sized patch, dry-coated with vaccine and applied via a simple spring-loaded applicator, can move doses out of refrigerators and infusion lines and into ordinary clinics—and eventually homes. Early clinical data with influenza suggest comparable or better immune responses at lower doses; separate usability work indicates that self-application is feasible and preferred—findings that, if borne out at scale, shift the economics of who delivers vaccines, where, and how fast.

What’s new under the hood

The capital raise is only half the story. Vaxxas already opened a 60,000-square-foot GMP facility in Brisbane designed to output “millions” of patches annually for late-stage trials and first commercial lots—unusual industrial readiness for a private clinical-stage vaccine-delivery company. The plant includes dual aseptic suites and device assembly lines, signalling an intent to control both biologic and device workflows typical of drug-device “combination products.”

On the science, the most consequential data point for payers and public health is thermostability. In January, CEPI advanced a US$4.8m program in which Vaxxas demonstrated, in preclinical work, that mRNA-LNPs printed onto the patch remained stable for at least 12 months at 2–8°C and 25°C, and for at least one month at 40°C—numbers that, if reproduced clinically, re-write last-mile planning. CEPI’s next step pairs Vaxxas with SK bioscience on a Japanese encephalitis mRNA candidate to build human data.

Clinical grounding (and its limits)

Randomised Phase 1 data in adults showed an influenza vaccine delivered by HD-MAP was safe and well tolerated, with evidence of dose-sparing and brisk antibody responses versus intramuscular injection. That is promising but still early; regulatory approval will require larger, strain-specific, head-to-head studies with clinical endpoints or validated correlates.

Separately, a 2023 human study (device coated with a tracer, not vaccine) found trained-user applications and self-applications were both feasible, safe and repeatable, with participants expressing a clear preference for patch delivery—useful signals for a future at-home model, but again not a substitute for efficacy data.

The competitive tableau: a quiet U.S.–Australia arms race

For U.S. readers, the relevant foil is Atlanta-based Micron Biomedical. In the last 18 months Micron secured CEPI support for “Disease X” preparedness, extended its Series A to $33m, and—crucially—kicked off what it calls the first CDC-sponsored clinic trial of a vaccine delivered by patch (rotavirus). It also reported positive measles–rubella (MR) patch data in toddlers and infants in The Gambia, with additional Gates funding to harden manufacturing. The picture is of two credible, differently capitalised platforms advancing in parallel, with U.S. agencies hedging bets.

That matters for money and policy. BARDA has now put a flag in Vaxxas as well, naming it a concept-stage winner in the $50m Patch Forward Prize—an initiative nested under the U.S. government’s Project NextGen to de-risk next-generation respiratory vaccines and delivery modalities. For a private Australian company, that’s a notable statement of U.S. strategic interest.

If patches scale, three cost centres bend

1) Cold chain. Dry-coated formulations that remain stable for months at ambient temperatures dilute refrigerant, storage and wastage costs. That isn’t merely a power bill; for LMIC campaigns, cold chain failure is a primary attrition point. (Caveat: preclinical stability claims must translate into real-world potency windows printed on labels.)

2) Labour and sites of care. Self-administration is not yet approved, but even task-shifting from physicians to pharmacists or community workers could lift throughput. Pandemic modelling suggests microarray patches can compress time-to-coverage materially—central for outbreak control where R₀ punishes delay.

3) Consumables and waste. Patches eliminate sharps and some PPE use. During COVID, syringes emerged as a rate-limiting input; any future surge vaccine will again collide with that constraint unless delivery is re-architected.

The regulatory reality check

Patches that deliver a biologic via a device are classic FDA “combination products.” That designation affects everything from lead-center assignment (typically CBER for vaccines) to cGMP integration and human-factors studies. Developers will need to run device-plus-vaccine programs, not device in isolation, and engage early on home-use claims. PATH’s target product profile for COVID MAPs explicitly warns that EUA pathways may not be available next time; groups should plan for full licensure with WHO PQ if targeting UN procurement. None of that is trivial—but it’s navigable.

Execution risks to watch (and how to report them)

Manufacturing: Vaxxas’s Brisbane facility is a differentiator, but “millions of patches per year” must be read against global demand measured in billions of doses. The near-term question is less can they make patches than at what cost per protected person versus vial-and-syringe—especially if dose-sparing holds. Track yield, line uptime, in-process controls and any scale-out beyond Brisbane.

Product-market fit: Which indications go first? Seasonal flu is the obvious proving ground in high-income markets; measles–rubella in LMICs is the humanitarian beachhead. Watch for registrational study designs that lock in public-health value (e.g., non-inferiority with operational advantages) rather than chasing marginal immunogenicity deltas.

Policy alignment: BARDA and CEPI are signalling that delivery platforms belong in the same breath as antigens. Follow Patch Forward stage-progression and CEPI’s 100-Day Mission milestones; budget lines today become procurement norms tomorrow.

The investable angle

If you are an investor, this is less a binary biotech bet than a supply-chain upgrade. The upside case is that one or more patch platforms achieve (a) label-printed room-temperature stability, (b) payor-accepted self-administration with remote verification, and (c) per-dose COGS that beat—or justify a premium over—needle-and-syringe once you price in logistics and labour. In that world, patches become the USB-C port of vaccination: a standard interface that shrinks adapters, speeds charging, and quietly changes user behaviour.

The base case is more prosaic: patches carve out specific, high-value niches—hard-to-reach campaigns, mass prophylaxis in outbreaks, or doses that benefit from skin-targeting—while the bulk of routine shots stay with syringes. The bear case is that device complexity, regulatory drag and real-world potency windows blunt the cost thesis.

Either way, Vaxxas just bought itself time to find out—and to prove that the economics of delivery can be as disruptive as the biology of the vaccine itself.